Building Systems, Not Making Decisions

The best financial decision you can make is to stop making so many. Here's how to build systems that handle the routine stuff so you can focus on what matters.

The best financial decision you can make is to stop making so many financial decisions.

That’s not a contradiction. It’s the logical endpoint of everything we’ve covered in this series. If decisions deplete you, if modern life demands too many of them, if research loops trap you and optimization exhausts you, then the answer isn’t to get better at deciding. The answer is to design your life so that fewer decisions land on your plate in the first place.

This is what behavioral economists call choice architecture, and you can use it on yourself.

The Power of Defaults

Researchers have long known that people tend to stick with whatever option is presented as the default. When companies switched 401(k) enrollment from opt-in to opt-out, participation jumped from around 49% to 86%. Same employees, same plan, same money. The only difference was which choice required action.

Defaults work because they remove the decision entirely. You don’t have to weigh options or summon willpower or find the perfect moment. The thing happens unless you actively stop it.

The question is whether your defaults are working for you or against you. Right now, the default on most of your subscriptions is “keep paying.” The default on your checking account is “sit there earning nothing.” The default on that gym membership you haven’t used in months is “renew automatically.”

You can flip this. You can set the default to the action you actually want to take, so that doing nothing is the same as doing the right thing.

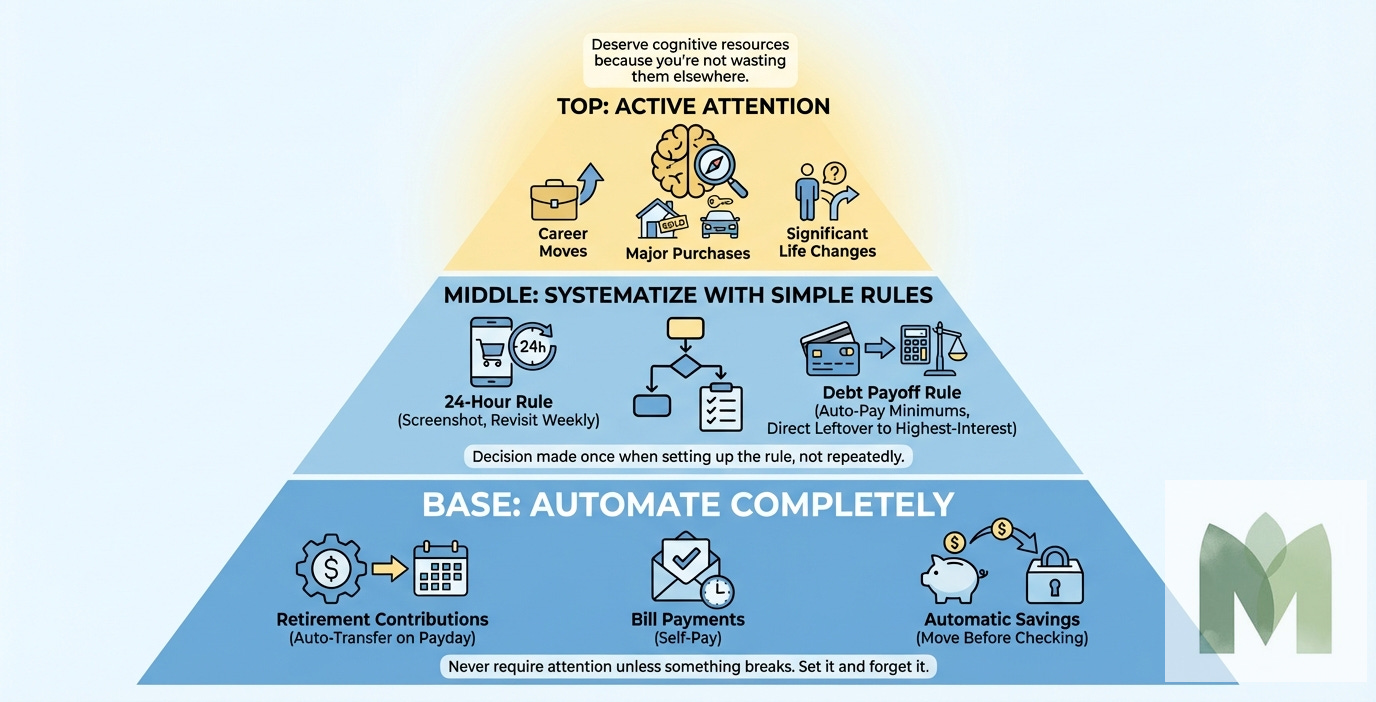

The Automation Hierarchy

Not every financial behavior needs the same level of attention. Some things benefit from active engagement, while others are better handled by systems that run in the background without your involvement.

At the base, you have decisions you should automate completely: retirement contributions that transfer automatically on payday, bills that pay themselves, savings that move to a separate account before you see the money in checking. These should never require your attention unless something breaks.

In the middle, you have decisions you can systematize with simple rules. Instead of asking “should I buy this?” every time you see something appealing, implement a 24-hour rule: take a screenshot of the item and revisit your screenshots once a week. Instead of wondering how much to put toward debt each month, you auto-pay minimums on everything and manually direct whatever’s left to the highest-interest balance. The decision is made once when you set up the rule, not repeatedly each time the situation arises.

At the top, you have the few decisions that genuinely benefit from your active attention, things like career moves, major purchases, or significant life changes. These deserve your cognitive resources precisely because you’re not wasting those resources on everything else.

The Gone Fishin’ Approach

Investor Alexander Green built an entire investment philosophy around this idea. He called it the Gone Fishin’ Portfolio, a simple mix of low-cost index funds designed to be set up once and rebalanced annually. The name says it all: you put your system in place, and then you go live your life, free from the mental drain of constantly monitoring, adjusting, and second-guessing.

The Gone Fishin’ Portfolio isn’t necessarily the right allocation for everyone, but the principle behind it applies universally. The best financial system is one that works without requiring your constant attention, turning a thousand small decisions into one bigger decision made upfront.

This is what “set it and forget it” actually means. Not neglect, but intentional design. You’re not ignoring your finances. You’re building a structure that handles the routine stuff so your attention stays available for what actually matters.

A Caution

Systems can enable avoidance if you’re not careful. The goal isn’t to eliminate all engagement with your money, because some level of awareness keeps you connected to your financial life and helps you catch problems early.

The goal is to free your attention for what matters by removing the friction of repetitive choices. Check in quarterly. Review your systems once a year. But between those check-ins, let the systems do their job.

One Thing to Try This Week

Pick one recurring financial decision that drains you and turn it into a system.

It could be automating a transfer to your savings account, so you no longer have to decide each month whether to save. It might involve setting up automatic payments for a bill that you often forget. Alternatively, you could establish a straightforward rule for a specific category of spending that causes you trouble.

One decision now, made deliberately, can eliminate dozens of future decisions you’d otherwise have to make while tired and distracted. That’s not avoiding responsibility. That’s taking responsibility seriously enough to design around your own human limitations.

You’ve now seen the full picture: why money decisions feel heavy, where the modern decision load comes from, how research loops trap you, why good enough beats perfect, and how systems can replace willpower. The thread running through it all is simple: you’re not broken. The demands are unreasonable, and you have more power to design your way out than you might think.

This content is for educational purposes only and should not be construed as financial or therapeutic advice. Consider speaking with qualified professionals for personalized guidance.