The Shame-Avoidance Spiral

Shame tells you to hide. Hiding makes things worse. Worse makes you feel more shame. Here's how to interrupt the loop.

There’s something underneath most financial avoidance that we haven’t named yet.

It’s not laziness, ignorance, or fear. It’s something more complex than that.

It’s shame.

Shame is subtle. It doesn’t make itself known. Instead, it makes you want to hide.

The Spiral

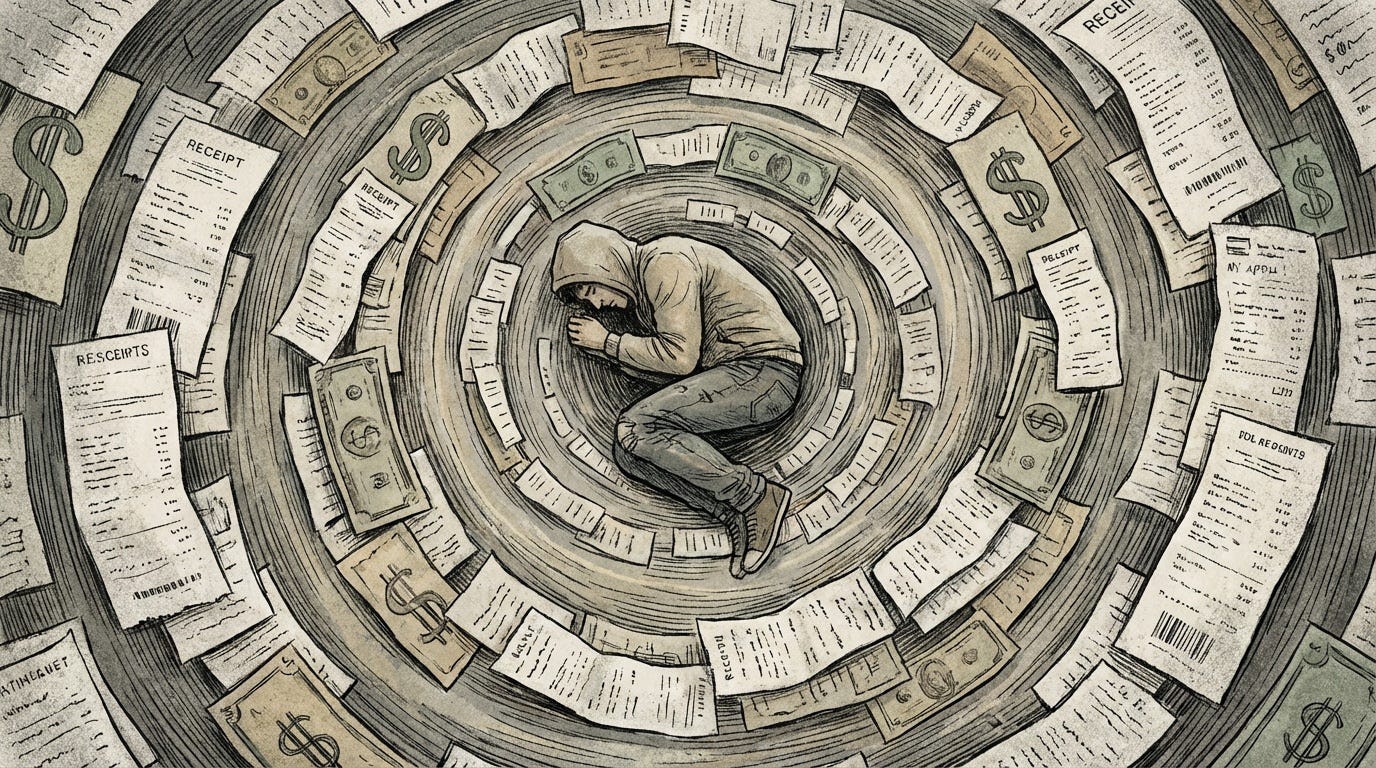

Researchers studied over 9,000 people to understand the relationship between shame and money. What they found was a loop. (Source: Gladstone, Jachimowicz, Greenberg, & Galinsky, “Financial Shame Spirals: How Shame Intensifies Financial Hardship,” Organizational Behavior and Human Decision Processes, 2021)

You feel ashamed about your finances. Shame makes you want to hide and avoid the situation, so you don’t look at it. Because you’re not looking, things get worse. You incur late fees, miss opportunities, and your balances grow. This creates more shame, which makes you want to hide even more. It goes round and round.

The cruel part? The hiding that shame demands is precisely what makes things worse. Shame says, “Protect yourself by disappearing.” But disappearing is what feeds the spiral.

Shame vs. Guilt

Here’s a distinction that matters more than you might think.

Guilt says: “I did something bad.”

Shame says: “I am bad.”

Guilt points at behavior. Shame points at identity.

This difference changes everything. Guilt can actually be useful. “I overspent this month” is something you can work with. You can make a different choice next time. Guilt allows for change.

But “I’m terrible with money”? “I’m irresponsible”? “I’m the kind of person who can’t get it together.”

That’s shame. And shame doesn’t motivate change. It motivates hiding.

When you believe the problem is who you are, looking at your finances feels like looking at proof of your failure. No wonder you’d rather not.

Debt and Shame

Debt carries a special weight.

Part of it is cultural. We live in a world that treats debt as a moral failure. “Good” people save. “Responsible” people don’t carry balances. The messages are everywhere, even when they’re not said out loud.

Part of it is personal. Debt often comes with a story—a hard season, a choice that made sense at the time, a slow accumulation you didn’t notice until it was big. But shame flattens all that context into a single verdict: you failed.

People hide debt from partners, family, and sometimes even themselves. The stigma is heavy enough that many would rather not know the exact number than face it.

If this is you, I want to say something clearly: Debt is not a character flaw. It’s a financial situation. Situations can change. The number in your account doesn’t define your worth.

Breaking the Loop

Here’s what shame doesn’t want you to know: it loses power when it’s spoken.

Shame thrives in isolation. It tells you that you’re the only one, that no one would understand, that people would think less of you if they knew. These are lies, but they’re convincing lies when you’re alone with them.

Research on shame consistently points to the same antidote: connection.

Not fixing the problem first. Not getting your finances in order and then talking about it. Connection while you’re still in it.

You could find a supportive friend, an open partner, a financial therapist, or an anonymous online community where people share their money experiences.

The first small truth breaks the seal. “I’ve been avoiding my credit card balance.” “I don’t actually know how much I owe.” “I’m scared to look.”

You don’t have to have answers. You don’t have to have a plan. You have to let one person see you in the mess.

What Now?

This one’s harder than the others. Noticing avoidance is one thing. Naming shame is another.

So here’s a gentle invitation, not a command:

Consider telling one person one small financial truth you’ve been keeping to yourself.

It doesn’t have to be the biggest thing. It doesn’t have to be your most profound shame. Start with something you can say out loud without your throat closing.

“I haven’t checked my bank account in three weeks.”

“I don’t really know where my money goes.”

“I have more debt than I’ve told you.”

You’re not alone in this, even when it feels that way. The spiral can be interrupted. And it usually starts with one honest sentence.

Next up: the smallest possible step. Because once you can see what you’re avoiding and understand why, there’s a path forward—and it’s much smaller than you think.

This content is for educational purposes only and should not be construed as financial or therapeutic advice. Consider speaking with qualified professionals for personalized guidance.